When Repo Rates Shift: The Ripple Effect on Home Loans and Property Demand

The repo rate is one of the most important measures used by central banks in order to manage the supply of money in the country, manage inflation, and support economic growth. Though the term may sound rather technical, a variation in the repo rate impacts the typical borrower in one way or another, mainly property investors and real estate developers.

A small rise or fall in the repo rate also tends to affect home loans, their rates of interest, and EMIs. Consequently, the demand for properties is also affected. Therefore, to make informed and intelligent decisions regarding finances, it is important to know and understand how such changes affect the home loan and real estate sectors.

Knowledge about Repo Rate

The repo rate, or the repurchase rate, is the interest rate at which the central bank lends money to commercial banks. It can be thought of as the base price of money. When the central bank changes the interest rate, it spills over effects on the economy regarding home loans.

- An increase in the repo rate increases the cost of Loans, and home loans tend to have higher interest rates.

- If the repo rate declines, it means that it becomes easier to borrow money. As a result, it becomes less expensive to get a home.

Usually, banks and financial organisations transmit these changes to their customers fairly soon, thereby meaning that any change in the repo rate is reflected in the interest rates offered on housing/retail loans.

Effect on Home Loan Rates of Interest

The interest rates for home loans are largely linked to the repo rates, especially after the repo rate-linked lending operations were initiated. A change in the repo rate leads to an equal change in the home loan rates.

1. When Repo Rates Rise

- Banks increase interest rates on home loans

- EMI payments for existing customers could see an increase every month

- The new borrowers are charged more for their borrowing

- Long-term borrowing is not as appealing

Higher EMIs may stretch the budget of the household, thus making the buyer wary of taking out a new home loan.

2. When Repo Rates Fall

- Interest rates on home loans come down

- EMIs fall, or loan tenures become shorter.

- Loans become cheaper for consumers

- Refinancing and balance transfer activity pick up.

Lower interest rates often spur the housing market, because such a policy encourages more people to purchase or upgrade their homes.

Impact on Property Demand

The impact of changes in the repo rate is not only felt in the EMI of the loan, but the repo rate also reflects its influence on the demand for properties in general.

● Increasing Repo Rates: The Demand Slows Down

If lendable funds become pricier to obtain, this will affect affordability. This leads to:

- First-time buyers could postpone their plans to buy

- Investors may consider other alternative investments

- The demand for prime or luxury properties may ease.

In order to sustain the level of sales, some discounts, convenient payment terms, or further incentives may be introduced by the developer.

● Decreasing Repo Rates: Demand Increases

Lower repo rates are generally expected to have a positive effect on the overall property market since:

- Consumer confidence increases

- The reduction in EMIs results in the enhancement of

- Homes will become more attainable for mid-income and first-time home buyers

This type of environment helps to produce an increased number of property transactions and an optimistic outlook within the property industry.

Real Estate Prices Influenced By

Repo rates will not affect property prices per se, though it impacts the overall behaviour of the market:

- Higher interest rates can induce a situation of stable or slow-growing prices.

- Lower interest rates could increase demand, thereby adding to a favourable environment in terms of price appreciation.

Over time, a steadily low rate of interest will attract both home buyers and investors, keeping the market active and, thus, competitive.

Impact on Developers and Construction Activity

Changes in the repo rate also have a large bearing on real estate developers:

- The rise in repo rates increases the cost of borrowing and project financing

- Repo rates are decreased, which enables funding as well as project feasibility.

If rates of interest are attractive, many developers resort to the inauguration of new projects, accelerating the building process, hence affecting the growth of the real estate industry positively.

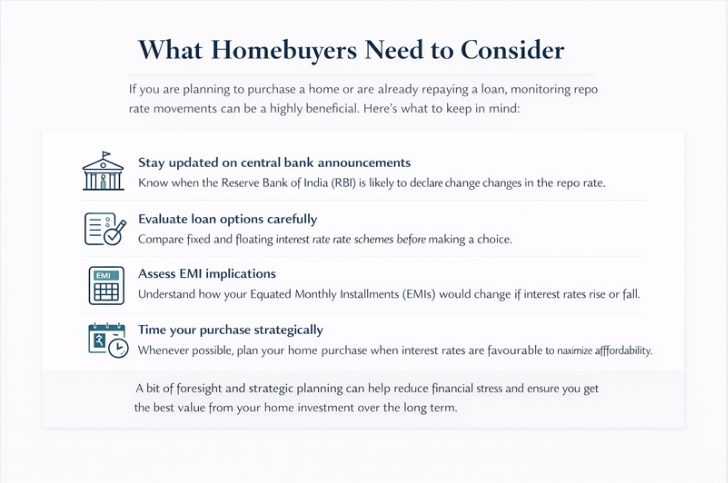

What Homebuyers Need to Consider

If you plan to purchase a house or are already on a loan, tracking the movements in the repo rate can help a great deal:

- Know when the central bank is going to declare the repo rate.

- Compare fixed and floating interest rate options before choosing one.

- See how your EMI would look in case of a rise or fall in interest rates.

- Where possible, time your purchase when interest rates are more favourable.

A little strategising can go a long way in saving you a lot of financial stress and getting the most value out of your home purchase in the long run.

Conclusion:

The repo rate affects an entire domain in the housing market, right from home loan affordability to buyer confidence and demand in the property market. Although an increased repo rate may slow down a market temporarily, a low repo rate brings with it energised and expansive growth in most markets. Home buyers, investors, and developers can make informed decisions in a constantly changing and shifting market by being aware of repo rate dynamics in their domain.